Big Banks and the U.S. Treasury Have Been Enabling Illegal Immigration for Two Decades

- External Source

admin

- 0

- 45 minutes read

Summary

-

After the 9/11 terrorist attacks dashed Mexico’s and the Bush administration’s hopes for a mass amnesty for illegal aliens, the Mexican government turned to a strategy of persuading federal, state, and local governments and the U.S. banking industry to accept Mexico’s matricula consular card for identification purposes for Mexican illegal aliens. Mexico’s goal was to achieve a de-facto amnesty by making it easier for illegal aliens to remain in the United States, especially by receiving banking services. This would also safeguard the continued flow of remittances back to Mexico.

- Mexico’s strategy was extraordinarily successful, facilitated by many U.S. banks’ desire to profit by turning millions of illegal aliens into customers. By the summer of 2003, more than 402 localities, 32 counties, 122 financial institutions, and 908 law enforcement agencies agreed to accept the matricula for identification purposes.

- The matricula fiesta was momentarily threatened by enactment of the “USA PATRIOT Act” in October 2001. The Act required the Treasury Department to issue regulations “requir[ing] financial institutions to implement … reasonable procedures for … verifying the identity of any person seeking to open an account”, with the goal of “provid[ing] the United States government with new tools to combat the financing of terrorism and other financial crimes”.

-

But the regulations that the Treasury Department actually wrote turned Congress’s intent on its head. By their own words, they did “not discourage bank acceptance of the ‘matricula consular’”. Why? The Treasury Department had readily admitted that it was trying “to find a balance between the need for strong regulation that provides a real benefit to those working to achieve national security and law enforcement objectives and the ability of financial institutions to serve non-U.S. persons” and that it was worried that “efforts to deter money laundering and disrupt terrorist financing … might have a negative impact on … encourage[ing] … non-U.S. persons living and working in the United States [read: illegal aliens] to use mainstream financial services”.

I am sorry that “efforts to deter money laundering and disrupt terrorist financing” might interfere with encouraging illegal aliens to use our banking system! These were not words written by President Obama’s Treasury Department — they were written by the Treasury of President George W. Bush, on whose watch the 9/11 terrorist attacks had occurred not long before.

As House Judiciary Committee Chairman F. James Sensenbrenner, Jr., wrote, “The intent of the Congress in directing the Treasury to write new regulations was to raise the bar on the difficulty with which terrorists can move money through the U.S. banking system. As written, the regulation appears instead to lower the bar.”

- Especially when the Trump administration is rightfully encouraging illegal aliens to “self-deport”, it makes absolutely no sense to keep Treasury Department regulations on the books that purposefully make it easier for illegal aliens to remain in the U.S. The misbegotten regulations, which should never have been promulgated in the first place, need to be repealed.

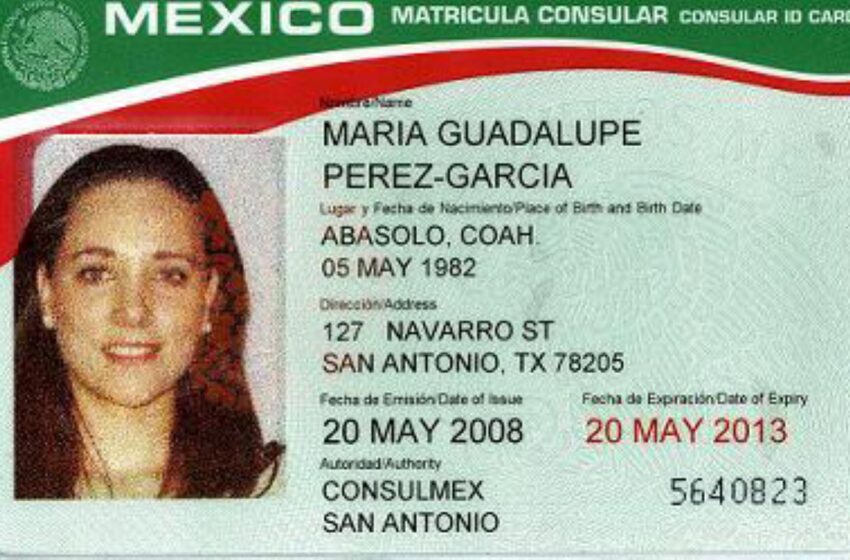

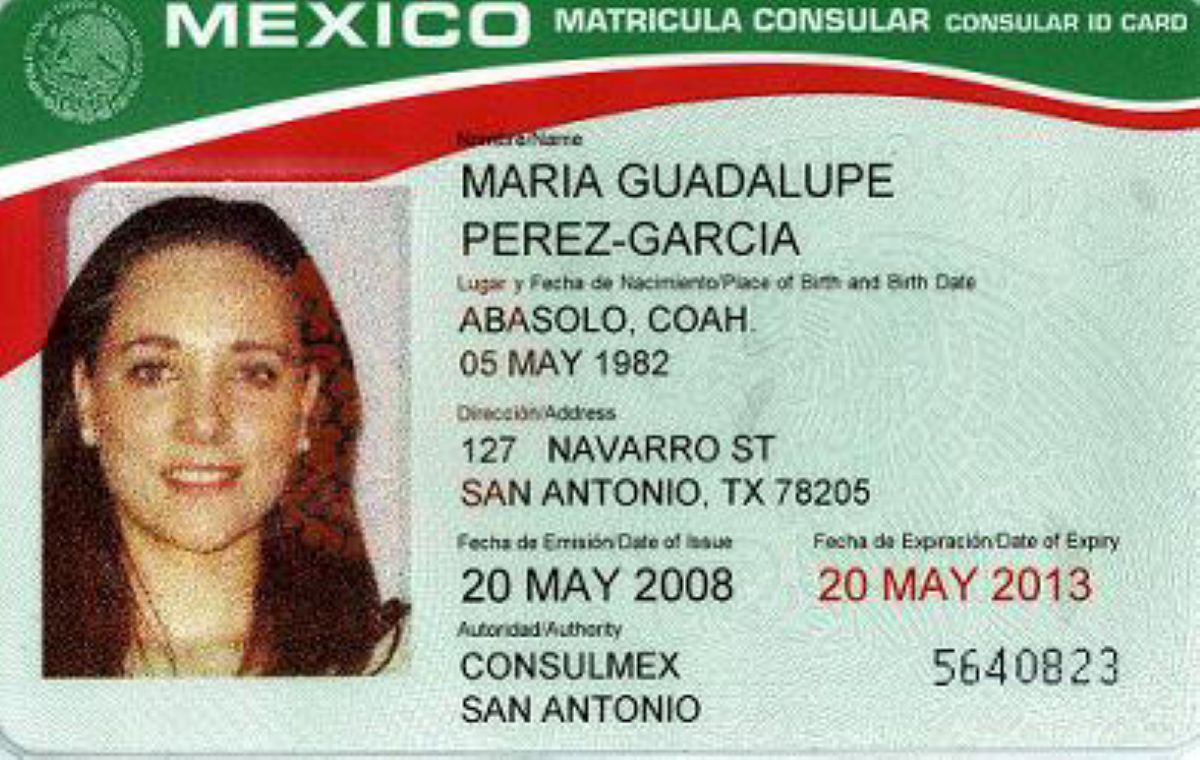

Mexican Matrícula Consular Cards and “Creeping Legalization”

The internet is awash in articles giving illegal aliens advice on where to do their banking. Last New Year’s Eve, Sophia Acevedo wrote a piece in Business Insider titled “Below, You’ll Find Some of the Banks that Accept Documents such as Foreign IDs if You’re Not a U.S. Citizen”. After opining that “Everyone should have access to fair banking tools and services regardless of their citizenship or immigration status,” she listed 27 “Top Banks for Immigrants and United States Non-Citizens” including Bank of America, Wells Fargo, and U.S. Bank. As to Bank of America, “You need to have two forms of ID with photos. For your primary ID, you can use a Canadian Citizenship Certificate Card, Foreign passport, Mexican Consular ID, Dominican Republic Consular ID, Colombian Consular ID, or Guatemalan Consular ID.”

Also included in the list were a number of “Juntos Avanzamos-Designated Credit Unions”. Pablo DeFilippi, executive vice president of the Inclusiv Network, stated that “To get the designation, you need to make sure that your policies and your procedures are welcoming and would enable someone, regardless of their immigration status to open an account and also access credit.” Acevedo added that “one of the requirements is to be able to accept alternative ID forms if you don’t have a U.S. ID”.

Wait a second, banks are allowed to accept foreign government IDs, such as Mexico’s infamous matrícula consular, to open bank accounts? Yes, indeed, all because of a regulation that the Bush administration’s Treasury Department issued in 2003 at the urging of the Mexican government and the banking industry.

The sorry story commenced in the aftermath of the 9/11 terrorist attacks. Roger Waldinger, professor of sociology at UCLA and director of the university’s Center for the Study of International Migration, explained that “The attack[s] … dashed until-then promising plans for a U.S.-Mexico deal on immigration. With ‘amnesty founder[-ing],’ Mexican leaders began looking for ways to ‘integrate [Mexican illegal alien] workers into U.S. locales’”.

What was Mexico’s strategy? Jorge Castaneda, the Mexican foreign minister at the time, explained that:

[We] began to try to obtain rights for Mexicans via other mechanisms, certainly less satisfactory than a migration accord, but significant and with direct effects on the daily life of millions of compatriots in the United States. The heart of this tactical turn consisted … in the expedition of the new matricula and political negotiations with banks and local authorities in the United States by our consuls in order to achieve the recognition of this matricula as an identity document[.]

What is the matricula consular? U.S. Rep. John Hostettler (R-Ind.), chairman of the House Judiciary Committee’s Subcommittee on Immigration, Border Security and Claims (at the time, I served as the subcommittee’s chief counsel), explained at a June 26, 2003, subcommittee hearing that:

[C]onsular cards have been issued for approximately 130 years … by consular officials to nationals abroad to allow those nationals to seek their home country’s assistance when they need help — for example, when they are injured or arrested.

Historically, therefore, the intended recipient of a consular card issued by a foreign government in the United States is the foreign government itself, not our Government and certainly not a locality in the United States.

But then, as Castaneda intimated, Rep. Hostettler explained at a June 19, 2003, hearing that:

-

Since early … 2002, however, those cards have served a new purpose. This is when the Mexican Government redesigned their consular identification card known as the Matricula Consular and began promoting it for local acceptance in the United States.

-

[Acceptance is] for identification purposes … at … police stops, to open bank accounts, to register for local services, to qualify for subsidized housing and even, reportedly, to board airplanes.

Over the past 2 years, more than a million and a half Matriculas have been issued by Mexican Government agencies in the United States.

And at the hearing on June 26, Chairman Hostettler stated that:

[W]hile the issuance of consular cards is a fairly old process, attempts by foreign government agents to lobby States and localities to accept the cards are not. None of the witnesses at last week’s hearing and no information that has come to the Subcommittee suggests that any foreign country issuing consular cards ever attempted to convince States or localities to accept those cards for domestic identification purposes before 2001.

Therefore, in the 130-year history of foreign government issuance of consular cards, foreign governments have only lobbied localities to accept those cards for the past 2 years.

Mexico’s goal was, as my colleague Mark Krikorian put it in 2003, “to bring about a de facto amnesty for illegal aliens”. Marti Dinerstein, president of Immigration Matters, testified at the June 19 hearing that: “The reason why government[s] want acceptance of their consular cards is to make it easier for their foreign nationals residing illegally in the U.S. to ‘come out of the shadows.’ It is in these governments’ interest for their illegals to remain in in the U.S. and remit money back to their home countries.” Chairman Hostettler stated at the June 26 hearing that “The foreign government’s only interest is the welfare of the alien, not the wellbeing of the American people.” U.S. Rep. Gary Miller (R-Calif.) stated in 2004 that “Mexico’s actions to advance acceptance by U.S. banks is a blatant attempt to make illegal immigrants in Mexico as inconspicuous as possible, while facilitating uninterrupted transmission [of] remittances back to Mexico.”

The Mexican government itself viewed things through exactly this lens. Waldinger wrote that “Mexico’s strategy” was “of ‘creeping legalization,’ as Casteneda described it”.

Waldinger continued:

[The strategy] built on its earlier decision to … “deliberately use [its consular offices] as channels to promote its interests”… [by] exploit[ing] openings in the fragmented US political structure … and to develop connections to Mexican Americans who could be converted into ethnic lobbyists. Having established ties to local stakeholders, whether inside or outside of government, and enjoying substantially augmented resources, the consulates quickly implemented the new tactic. As Casteñeda explains … “every Mexican consul was instructed to negotiate with local banks, city officials, police departments, lawyers, etc. to persuade them to accept or ‘recognize’ the [matricula consular] as an official document.”

Mexico’s drive was amazingly successful. Chairman Hostettler noted at the June 19 hearing that “to date, more than 402 localities, 32 counties, 122 financial institutions and 908 law enforcement agencies accept the Matricula for identification purposes”.

As to U.S. banks, Kathryn Lee Holloman wrote in the North Carolina Banking Institute that “Competition among [Wells Fargo, Bank of America and Citigroup] reached an all-time high in the spring of 2002, as all three began accepting the Matricula Consular as a primary form of identification to open a bank account, thus abandoning the previous policy that primary identification be a document issued by the U.S. government.” She concluded that banks’ motivation was clear — they “want[] to profit from the large, and virtually untapped, economic market surrounding the transfer of funds from Mexican nationals”.

Graham Gori explained in the New York Times on July 6, 2002, that:

-

For years, the banks had refused service to most Mexican immigrants because they could not verify their identities.

-

Mexico’s government hopes that with access to banks, its citizens will find cheaper vehicles than money-transfer businesses for sending billions of dollars in remittances to relatives back home. United States banks hope to reach out to the large and growing number of Hispanics … .

“If we’re to be successful and continue to grow, we’re going to have to become the bank of choice for the Hispanic community,’” said Jeffrey Bierer, a spokesman for Bank of America. Undocumented Mexican immigrants, he said, make up a large chunk of that community.

“It is a significant market now,” he said. “It’s growing every year.”

-

[Bank of America] is one of some 60 banks nationwide … that have begun catering to illegal immigrants.

-

“Right now it’s like a landslide — the bankers come to us,” said Enrique Berruga, undersecretary for foreign affairs in Mexico’s foreign ministry.

Waldinger wrote of the rollout of Mexico’s strategy:

Proactive [Mexican] consuls persuaded the financial sector, already interested in the rapidly expanding immigrant market, that the matrícula could prove advantageous. In November 2001, Wells Fargo began accepting the consular card as identification for new accounts … [which] Mexico’s then consul in Los Angeles described as her greatest achievement. … Citibank and the Bank of America soon followed suit. … By fall 2003 customers using the matrícula had opened almost a quarter of a million accounts at Wells Fargo. … Following a 2004 closed-door meeting between top US bank leaders and then President Vicente Fox, the banks gained permission to market their products throughout all of Mexico’s consulates in the United States. … Later, Bank of America began covering part of the costs of Mexico’s mobile consulates, in return for getting a venue for “bank employees to pitch its SafeSend remittance service and other banking products.”

At the June 19 hearing, U.S. Rep. Lamar Smith (R-Texas) asked witness Craig Nelson, director of Friends of Immigration Law Enforcement, “Do you think that some banks might put a few dollars profit ahead of homeland security?” Nelson responded that “I think profit motive is clearly taking precedence here.” Smith responded that “I think they are being shortsighted and might be tempted to put the profits ahead of what is good for the country in the long run.” In 2004, Smith stated on the House floor “We simply should not put the private interests of a few financial institutions ahead of the public good and the security of the American people.”

Why Matrículas Matter

Illegal Immigration

As Mark Krikorian explained in 2002, the acceptance of the matricula “makes life easier for illegal immigrants, and that compromises law enforcement and security . . . It’s a creeping amnesty that incorporates illegal aliens into our institutions.” Sam Dillon reported in the New York Times on March 15, 2003, that:

Immigration experts said the widespread acceptance of the ID was a watershed in the lives of millions of Mexicans who work in the United States without valid immigration documents and previously lacked any legal identification. The card allows them not only to obtain banking services, but also to participate more fully in American life in ways like reporting crimes, traveling on planes and renting videos.

Specifically as to acceptance by banks, Dinerstein explained in an article for the Center for Immigration Studies that:

Some Mexican illegals view a banking relationship as the most important tangible value of the matricula consular. For those who work off the books, it provides peace of mind to know they no longer are easy marks for thieves who prey on people who fear going to the police. For others, it makes cashing paychecks easier. Not only does it reduce the cost of sending money to their homes in Mexico, it provides these families with an ATM card, so they can withdraw only enough cash to meet their needs and keep the rest secure in a bank.

Holloman stated, “The Mexican government, recognizing this de facto amnesty, actively encourages local governments to accept the Matricula Consular in an effort to integrate undocumented aliens into the U.S. mainstream.” And she noted that “having a bank account is as essential as having electricity, running water, and telephone service” and thus that “the ramifications of being unbanked are far reaching. Mexican nationals with access to financial institutions such as banks may find that it is easier to rent homes, buy homes, and obtain car loans.”

Lamar Smith explained in 2004 that “Giving illegal immigrants an identification card encourages them to come to the United States and, of course, makes it easier for them to stay.” At the June 19 hearing, he stated that:

[A]ll of those who would argue in favor of the use of this consular identification card are basically arguing or saying that they are in favor of it because they want to make it easier for illegal immigrants to stay in America.

Those of us who oppose the card are opposed to it for that exact same reason, because it does make it easier for those who have broken our immigration laws to remain in the country.

[W]hen you make it easier for individuals to have bank accounts … and so forth, not only are you making it easier for them to stay in the country, but you are actually encouraging illegal immigration. Because the message that is sent is, come into the country, even if it is illegally, and we are going to make life easier for you once you get here.

Security Concerns

Rep. Smith explained at the June 19 hearing that “the real issue [with the matricula consular] … is … the use of underlying fraudulent documentation or the ability of individuals to get multiple consular identification cards”. Steven McCraw, assistant director of the FBI’s Office of Intelligence, testified at the June 26 hearing that:

-

[I]n order to protect the American people, we must be able to determine whether an individual is who he purports to be. This is essential in our mission to identify potential terrorists.

-

The Department of Justice and the FBI have concluded that the Matricula Consular is not a reliable form of identification, due to the non-existence of any means of verifying the true identity of the card holder. The following are the primary problems with the Matricula Consular that allow criminals to fraudulently obtain the cards:

First, the Government of Mexico has no centralized database to coordinate the issuance of consular ID cards. This allows multiple cards to be issued under the same name, the same address, or with the same photograph.

Second, the Government of Mexico has no interconnected databases to provide intra-consular communication to be able to verify who has or has not applied for or received a consular ID card.

Third, the Government of Mexico issues the card to anyone who can produce a Mexican birth certificate and one other form of identity, including documents of very low reliability. Mexican birth certificates are easy to forge and they are a major item on the product list of the fraudulent document trade currently flourishing across the country and around the world. A September 2002 bust of a document production operation in Washington state illustrated the size of this trade. A huge cache of fake Mexican birth certificates was discovered. It is our belief that the primary reason a market for these birth certificates exists is the demand for fraudulently-obtained Matricula Consular cards.

Fourth, in some locations, when an individual seeking a Matricula Consular is unable to produce any documents whatsoever, he will still be issued a Matricula Consular by the Mexican consular official, if he fills out a questionnaire and satisfies the official that he is who he purports to be.

In addition to being vulnerable to fraud, the Matricula Consular is also vulnerable to forgery … [as] even the newest version can be easily replicated, despite its security features.

McCraw went on to state that “there are two major criminal threats posed by the cards, and one potential terrorist threat”:

-

The first criminal threat stems from the fact that the Matricula Consular can be a perfect breeder document for establishing a false identity. … Individuals have been arrested with multiple Matricula Consular cards in their possession, each with the same photograph, but with a different name. … [F]alse identities are particularly useful to facilitate the crime of money laundering, as the criminal is able to establish one or more bank accounts under completely fictitious names. Accounts based upon such fraudulent premises greatly hamper money-laundering investigations once the criminal activity is discovered.

The second criminal threat is that of alien smuggling. … Federal officials have arrested alien smugglers who have had as many as seven different Matricula Consular cards in their possession.

-

The ability of foreign nationals to use the Matricula Consular to create a well-documented, but fictitious, identity in the United States provides an opportunity for terrorists to move freely within the United States without triggering name-based watch lists that are disseminated to local police officers.

The USA PATRIOT Act

The matricula fiesta was momentarily threatened by the “USA PATRIOT Act”, enacted into law on October 26, 2001. Section 326 — “Verification of Identification” — mandated that “the Secretary of the Treasury shall prescribe regulations setting forth the minimum standards for financial institutions and their customers regarding the identity of the customer that shall apply in connection with the opening of an account at a financial institution”. The section originated in the “Financial Anti-Terrorism Act of 2001” (H.R. 3004), introduced by Rep. Michael Oxley (R-Ohio), chairman of the House Financial Services Committee. The committee’s report on H.R. 3004 stated that that bill’s overarching purpose was to “provide[] the United States government with new tools to combat the financing of terrorism and other financial crimes. The legislation contains provisions to strengthen law enforcement authorities, as well as enhance public-private cooperation between government and industry in disrupting terrorist funding.”

Section § 326 provided that:

The regulations shall, at a minimum, require financial institutions to implement, and customers … to comply with, reasonable procedures for—

(A) verifying the identity of any person seeking to open an account to the extent reasonable and practicable;

(B) maintaining records of the information used to verify a person’s identity, including name, address, and other identifying information; and

(C) consulting lists of known or suspected terrorists or terrorist organizations provided to the financial institution by any government agency to determine whether a person seeking to open an account appears on any such list. [Emphasis added.]

Section 326 added that “In prescribing [such] regulations … the Secretary shall take into consideration the various types of accounts maintained by various types of financial institutions, the various methods of opening accounts, and the various types of identifying information available.” It also gave the secretary the power to “exempt any financial institution or type of account from the requirements of any regulation prescribed … in accordance with such standards and procedures as the Secretary may prescribe”.

In addition, § 326 required the secretary to submit a report to Congress containing recommendations for:

(1) determining the most timely and effective way to require foreign nationals to provide domestic financial institutions and agencies with appropriate and accurate information, comparable to that which is required of United States nationals, concerning the identity, address, and other related information about such foreign nationals necessary to enable such institutions and agencies to comply with the requirements of this section;

(2) requiring foreign nationals to apply for and obtain, before opening an account with a domestic financial institution, an identification number which would function similarly to a Social Security number or tax identification number; and

(3) establishing a system for domestic financial institutions and agencies to review information maintained by relevant Government agencies for purposes of verifying the identities of foreign nationals seeking to open accounts at those institutions and agencies.

The committee report on H.R. 3004 (there were no committee reports for the USA PATRIOT Act) explained that:

-

It is the Committee’s intent that the verification procedures prescribed by Treasury make use of information currently obtained by most financial institutions in the account opening process. It is not the Committee’s intent for the regulations to require verification procedures that are prohibitively expensive or impractical.

-

Current regulatory guidance instructs depository institutions to make reasonable efforts to determine the true identity of all customers requesting an institution’s services. … The Committee intends that the regulations … adopt a similar approach, and impose requirements appropriate to the size, location, and type of business of an institution.

The Treasury Department’s Report

Kathryn Lee Holloman wrote that “[i]nitially, it appear[ed] that the Department of the Treasury was prepared to impose heavy responsibilities on various financial institutions” in the regulations. But then, on October 21, 2002, the Treasury issued the report required by § 326, and essentially admitted that a prime goal was to actually facilitate illegal aliens’ access to our banking system — even at the expense of national security:

[T]he recommendations in this report reflect Treasury’s recognition of the importance of providing non-U.S. persons with access to the financial system and its effort to find a balance between the need for strong regulation that provides a real benefit to those working to achieve national security and law enforcement objectives and the ability of financial institutions to serve non-U.S. persons living and working in the United States. [Emphasis added.]

Did the Treasury Department really admit to Congress that it wanted to “balance” national security and law enforcement with “the ability of financial institutions to serve non-U.S. persons”? Yes, even though the department later acknowledged in its proposed regulations that “the main purpose of the [USA PATRIOT] Act is to prevent and detect money laundering and the financing of terrorism”. Treasury’s report further revealed in a section titled “Balancing of anti-money laundering concerns and efforts to move the unbanked population, including foreign nationals, into the banking system” that:

In its efforts to deter money laundering and disrupt terrorist financing, Treasury is cognizant that additional regulatory burdens on financial institutions might have a negative impact on other Treasury programs, such as the initiative to encourage “unbanked” families and individuals, including non-U.S. persons living and working in the United States, to use mainstream financial services. In addition to discouraging the unbanked from using mainstream financial services, imposing burdensome requirements with respect to non-U.S. customers could discourage financial institutions from serving these populations as such institutions already face special challenges in complying with identification requirements because many of their customers may not have standard forms of U.S. identification.

With such a mindset, it comes as no surprise that the report stated that “the proposed regulations do not discourage bank acceptance of the ‘matricula consular’ identity card that is being issued by the Mexican government to immigrants.”

I am sorry that “efforts to deter money laundering and disrupt terrorist financing” might interfere with “encourage[ing] ‘un-banked’ … non-U.S. persons” to use our banking system! And this was not a report written by President Obama’s Treasury Department — it was written by the Treasury of President George W. Bush, on whose watch the 9/11 terrorist attacks occurred just a year earlier!

Of course, the “non-U.S. persons” the Treasury Department was referring to were primarily illegal aliens. The report stated that:

The millions of undocumented aliens and aliens who entered the United States without inspection (“EWI”) are not in any records system of the [Immigration and Naturalization Service] INS. … Only those illegal/undocumented aliens and EWIs who have been arrested, detained, or put in removal proceedings by INS are in the current databases. The vast majority of illegal/undocumented aliens and EWIs, however, are in no INS database. … As a result, it would not be uncommon to find that a foreign national opening an account at a financial institution is not in any INS database.

It was widely understood at the time that only Mexican illegal aliens needed its matricula consular for purposes of dealing with the U.S. government and immersing themselves in the U.S economy.

Rep. Hostettler stated at the subcommittee’s June 19 hearing that “With limited exceptions, all aliens who are legally present in the United States possess either U.S. Government issued cards or passports. … Critics have argued, therefore, that the only aliens in the U.S. [w]ho need … additional identification documents … are those who are illegally here.” And he explained at the June 26 hearing that “it appears that those countries [that issue consular cards] acknowledge the fact that most of the aliens applying for those cards in our country are here illegally and need the card because they have no form of lawful identification”.

And Steven McCraw testified at the June 26 hearing that:

It is believed that consular ID cards are primarily being utilized by illegal aliens in the United States. Foreign nationals who are present in the U.S. legally have the ability to use various alternative forms of identification — most notably a passport — for the purposes of opening bank accounts, gaining access to federal facilities, boarding airplanes, and obtaining a state driver’s license.

At that hearing, Stewart Verdery, assistant secretary for policy and planning, Border and Transportation Security Directorate, Department of Homeland Security, was asked by now-Sen. Marsha Blackburn (R-Tenn.) “[W]ho needs a Matricula Consular card other than an illegal alien in the United States?” Verdery responded “if you are here legally … you would either have a passport with a visa; you would have a Border Crossing Card if you were a frequent traveler that is basically the equivalent of a visa, or you would have a Permanent Residency Card.”

The Treasury Department Regulations

On July 23, 2002, the Treasury Department issued its proposed regulations, which, true to the word of Treasury’s report, did “not discourage bank acceptance of the ‘matricula consular’”. As to the matricula, the regulations provided that:

[A]t a minimum, a bank must obtain the following information prior to opening … an account. … For non-U.S. persons, one or more of the following: a U.S. taxpayer identification number; passport number and country of issuance; alien identification card number; or number and country of issuance of any other government-issued document evidencing nationality or residence and bearing a photograph or similar safeguard. [Emphasis added.]

They explained that “Rather than imposing the same list of specific requirements on every bank, regardless of its circumstances, the proposed regulation requires all banks to implement a Customer Identification Program (CIP) that is appropriate given the bank’s size, location, and type of business.” Further:

[E]ach bank must have risk-based procedures for verifying the identity of a customer that take into consideration the types of accounts that banks maintain, the different methods of opening accounts, and the types of identifying information available. These procedures must enable the bank to form a reasonable belief that it knows the true identity of the customer.

Holloman concluded that:

The proposed rules … fail to support the overwhelming movement to fight money laundering … . [R]ather than mandating strict requirements for customer identification programs for financial institutions, the proposed rules adopt a flexible “reasonable procedure” approach to customer identification … .

It has been suggested, however, that a more detailed and uniform procedure is necessary for verifying customer’s identification.

The banking industry launched a lobbying campaign to ensure that the final rule would not deviate from this path. Waldinger noted that “As described by the American Banker the banking industry went ‘on the offensive’ … opposing any move to limit the [matricula’s] use.”

On May 9, 2003, Treasury promulgated the final rule (with the regulations now located at 31 C.F.R. § 1020.220). Waldinger wrote that “Ultimately, Treasury decided not to recommend any further changes, much to the satisfaction of both banks and the Mexican government.” The final rule explained that it “provide[d] a bank with some flexibility to choose among a variety of identification numbers that it may accept from a non-U.S. person”, “because there is no uniform identification number that non-U.S. persons would be able to provide to a bank”.

The rule itself stated that “The majority of comments received … were from banks, savings associations, credit unions, and their trade associations.” Big surprise! “Most of these commenters agreed with the largely risk-based approach set forth in the proposal that allowed each bank to develop a CIP based on its specific operations.” Big surprise! “[S]ome … commenters recommended that Treasury … adopt an entirely risk-based approach without any minimum requirements.” Big surprise! The rule added that the proposed rule had gotten a pat on the back from “[c]ommenters representing certain consumer advocacy groups [who] commended Treasury … for providing banks with the discretion to accept alternative forms of identifying information from non-U.S. citizens. These commenters stated that this position would assist low-income [read: illegal] immigrants in gaining financial stability.”

The rule stated that “Treasury … emphasize[s] that the final rule neither endorses nor prohibits bank acceptance of information from particular types of identification documents issued by foreign governments. A bank must decide for itself, based upon appropriate risk factors … whether the information presented by a customer is reliable.” Wait, shouldn’t that have been the job of the regulations — to tell banks which types of information were reliable? As Holloman wrote:

[T]he proposed rules … provide no definite guidelines for banks to follow. Ultimately, these lax requirements defeat the underlying purpose of the Patriot Act: to curb money laundering.

The danger in failing to establish such procedures is that banks are left to their own discretion in determining what constitutes a reasonable procedure. The opportunity to venture into the $9.2 billion dollar market for wire transfers from Mexican nationals in the United States could skew a bank’s definition of “reasonable”. The acceptance of the Matricula Consular reflects the growing desire among banks to enter this marketplace.

And she noted that “Moreover, banks are reluctant to impose higher identification requirements than competing banks for fear of placing themselves at a potential disadvantage.” This is not just a theoretical concern. Sophia Acevedo wrote that:

[Pablo] DeFilippi says to be persistent while searching for financial products and services, even if you’re initially turned away because of your immigration status.

“It takes courage to get out and approach a financial institution., but I think that is critical that we all do that,” said DeFilippi. “If someone says no to you, go someplace else.”

Among other highly questionable policies, the final rule stated that a “bank generally may rely on government-issued identification as verification of a customer’s identity; however, if a document shows obvious indications of fraud, the bank must consider that factor in determining whether it can form a reasonable belief that it knows the customer’s true identity”. (Emphasis added.) Wait, a bank is not precluded from “reasonabl[y] belie[ving] that it knows the customer’s true identity” because said customer provides a document “show[ing] obvious indications of fraud”? The bank just has to “consider” such indications of fraud?

And the rule stated that it “does not specifically require a bank to close the account of a customer whose identity the bank cannot verify, but instead leaves this determination to the discretion of the bank”. What?

Critics’ Response

On May 23, 2003, Rep. F. James Sensenbrenner, Jr., chairman of the House Judiciary Committee, sent a letter to Dr. Richard Falkenrath, assistant director of the White House’s Homeland Security Council, stating that:

-

I am writing to request that the Executive Office of the President direct that the final date of th[e] regulation be postponed for six months until scrutiny by law enforcement officials can be more intensively applied to modify it. The intent of the Congress in directing the Treasury to write new regulations was to raise the bar on the difficulty with which terrorists can move money through the U.S. banking system. As written, the regulation appears instead to lower the bar.

There are numerous instances within the legislative language of that regulation that appear to have the potential for hindering the successful investigation of potential terrorists and of organizations supporting terrorism through financial means. The two specific regulatory conditions that are of greatest concern [include]:

-

Pursuant to the final regulation … a bank may open an account for an alien who presents only … “number and country of issuance” of any … government-issued document evidencing nationality or residence and bearing a photograph or similar safeguard.

This is a significant step backward from requiring that aliens present a passport, which is the pre-existing standard for non-U.S. citizens presenting identification to open accounts in U.S. banks. Passports, because of the existing treaties under United Nations’ auspices, have many safeguards for identification, and there is an existing body of international law and United States Code that addresses security features of passports.

In an attempt to assuage Sensenbrenner, on July 1, 2003, the Treasury published a Notice of Inquiry in the Federal Register stating that:

The Department of the Treasury seeks additional comments from all interested persons on two discreet issues relating to financial regulations issued recently … [including] whether there are situations when the regulations should preclude reliance on certain forms of foreign government-issued identification to verify customer identity.

Treasury … emphasized that the final rules neither endorsed nor prohibited a financial institution’s acceptance of particular types of identification documents issued by foreign governments … .

Ensuring the appropriate identification of all persons opening accounts at financial institutions, including non-U.S. citizens, is a significant goal of the final regulations. Therefore, Treasury seeks additional comment on whether there are situations in which the regulations should preclude reliance on certain forms of foreign government-issued identification to verify customer identity … .

1. Should the regulations preclude financial institutions’ reliance on certain forms of identification issued by certain foreign governments?

2. Should the regulations require financial institutions to obtain a passport number from all customers who are non-U.S. citizens? …

3. Is there sufficient empirical information to enable Treasury to assess the utility of the various forms of foreign-issued identification for purposes of accurately identifying the holder?

4. What would the impact be on the use of the conventional financial system if financial institutions were prohibited from accepting certain forms of government-issued identification?

The views of law enforcement, the industry, and others are sought, even if such views have been expressed previously in connection with the proposed rulemakings.

On September 18, 2003, the Treasury announced the results of its Notice of Inquiry. “After reviewing over 34,000 comments, Treasury found that no new information had been presented that had not been considered prior to issuing the final rules. Accordingly, Treasury is recommending no changes to the rules.” Really, “no new information”? I assume the whole exercise was simply a charade.

In 2004, congressional critics sought to shut down the regulations. Section 216 of H.R.5025, the “Departments of Transportation and Treasury and Independent Agencies Appropriations Bill, 2005”, as reported by the House Appropriations Committee, provided that “None of the funds made available in this Act to the Secretary of the Treasury may be used to publish, implement, administer, or enforce regulations that permit financial institutions to accept the matricula consular identification card as a form of identification.”

An attempt to strike § 216 during the Appropriations Committee’s markup of the bill failed by a vote of 25-26. But, as Waldinger wrote, the “Banks successfully fought back.” On the House floor, Chairman Oxley offered an amendment to strike § 216.

U.S. Rep. Dana Rohrabacher (R-Calif.) stated during floor debate that:

-

This is the quintessential example of an interest group … this time, financial interest groups, the banks, et cetera, putting themselves over the well-being of our country. … [W]e are talking about an interest group putting its self-interests, its profits above the safety of our country. Yes, it would make it easier for these banks to do business with illegal immigrants, and they would make a profit from it; but our country would be far less safe, and our children will be less safe if we do this.

-

What we have got here is an effort to make it easier for illegal immigrants to stay in this country and to be in this country at the expense of the safety of our very people.

-

These financial institutions are putting themselves above the well-being and safety of the United States of America, and that is what this amendment is all about.

And U.S. Rep. Gary Miller (R-Calif.) stated that “No matter how we spin it, the fact of the matter is this amendment is not about banking, it is about making it easier for illegal immigrants to remain in the United States.”

The Oxley amendment was approved by a vote of 222-177 (Republicans voted 49-161, Democrats 172-16).

Conclusion

Secretary of Homeland Security Kristi Noem announced in May that:

If you are here illegally, self-deportation is the best, safest and most cost-effective way to leave the United States to avoid arrest. DHS is now offering illegal aliens financial travel assistance and a stipend to return to their home country through the CBP Home App[.] This is the safest option for our law enforcement, aliens and is a 70% savings for US taxpayers. Download the CBP Home App TODAY and self-deport.

Especially when the Trump administration is rightly encouraging illegal aliens to “self-deport”, it makes absolutely no sense to keep Treasury Department regulations on the books that purposefully make it easier for illegal aliens to stay. The misbegotten regulations, which should never have been promulgated in the first place, need to be repealed.